Ending the practice of court debt-based driver’s license suspensions is a pressing matter for the Fines and Fees Justice Center but they need your help to reach this goal. Please take a few minutes to complete and share their License Suspension Survey (link below):

https://docs.google.com/forms/d/e/1FAIpQLSeZGZ18eE7dFaij46SOYrUnemXYh97dA15ypB9wwSiDvt1QVQ/viewform

Too Poor to Drive: 6 Truths about Driver’s License Suspension

Truth #1: Debt-based driver’s license suspension affects millions of families nationwide.

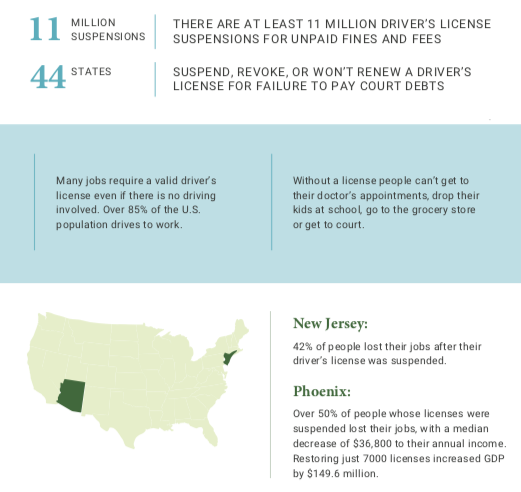

- Across the country, 44 states suspend driver’s licenses over unpaid fees, fines, or other debts. Nationwide there are least 11 million driver’s license suspensions for unpaid fines and fees. Research suggests that 40% of license suspensions are for unpaid traffic tickets, unpaid child support, or drug offenses.

- All kinds of debts can trigger a license suspension, including amounts of money owed from parking tickets, traffic fines, and court costs. As of 2017, 20 states even revoked state-issued licenses over student loans. In South Dakota,

nearly 1,000 residents cannot hold a driver’s license because they owe money to state universities. In short, debt-based driver’s license suspension can—and does—affect everyone.

nearly 1,000 residents cannot hold a driver’s license because they owe money to state universities. In short, debt-based driver’s license suspension can—and does—affect everyone.

Truth #2: Debt-based driver’s license suspension reduces public safety.

- When we suspend driver’s licenses for unpaid debts, we make our communities less safe. Every moment that we spend arresting and prosecuting the poor for unpaid debt is a wasted moment that doesn’t promote public safety.

- Studies have found that the states waste an average of nine hours for all roadside stop-related activities when someone is caught driving with a suspended, revoked, or canceled the license. In 2015, it’s estimated that Washington State spent over 70,848 hours addressing license suspensions for non-driving offenses. These hours represent thousands of hours spent detaining and questioning individuals who pose no risk to public safety and millions of dollars wasted.

- A recent study found that a 1% increase in debt-based revenues—money from fees, fines, and forfeitures—is associated with a 3.7% decrease in violent crimes being solved. A city attorney of Minneapolis reported that 30 percent of her office’s caseload was spent on license suspension and revocation cases. As one Tennessee district attorney put it, describing his decision to stop prosecuting many driver’s license violations, “I only get 65 ADAs. I want them working on violent crime.”

Truth #3: Debt-based driver’s license suspension hurts people’s ability to repay their debts.

- Many professions—including automotive technician, cable installation technician, caregiver, construction worker, housecleaner, HVAC technician, landscaping crew member, maintenance worker, plumber, pressure washer, truck washer, unarmed security officer, and warehouse worker—directly require people to drive. In one survey, 80% of respondents reported that they had no access to or were unqualified for job opportunities because of license suspension.

- Even when the job doesn’t directly require a car, not having driving privileges makes getting to work impossible. In Tennessee, for example, more than 9 of every 10 people—93% of drivers statewide—drive to work. Even in metropolitan Memphis, Nashville, and Knoxville, approximately 75% of jobs are not reasonably accessible by public transportation.

- In New Jersey, 42% of drivers lost their jobs once their driving privileges were suspended. Of those drivers, nearly half could not find new employment. And, of those that did, nearly 9 in 10 reported a loss in income.

- Phoenix launched a program that helped drivers repay their debts using payment schedules appropriate to their budgets. More than half of the participants had lost their jobs post-license suspension, causing a $36,800 loss in median income. After regaining their licenses, more than 40% reported an increase in income, the median increase being $24,000. Phoenix raised $149.6 million in revenue during the nine-month study—just by letting people drive.

- Eliminating debt-based driver’s license suspension does not eliminate the underlying debt. It just makes it easier for people to pay the money that they owe.

Truth #4: Debt-based driver’s license suspension has catastrophic effects on individuals and their families.

- People affected by debt-based license suspension can’t do the simple things that most people take for granted. They can’t drive to school, go to church, visit loved ones, go to the doctor, or take care of their children. For one man who ultimately had his license restored, Johnny Gibbs, this restoration was life-changing—for him and his daughters. When explaining why he began to cry. “I’m a blue-collar guy,” Gibbs said. “I try to keep my emotions in, but my kids are my world. I’ve missed Thanksgivings, Christmases, birthdays. Now that distance is not going to be an issue.”

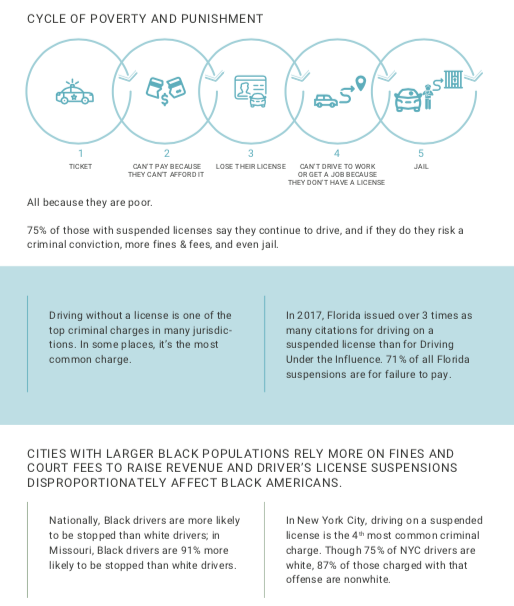

- Studies show that 75% of individuals continue driving even after their licenses have been suspended. This means that each year, debt-based license suspensions expose millions to cascading consequences that include jail time and more debt from fees. In Cook County, people arrested because they drove on a suspended license spent, on average, 14 days in jail.

Truth # 5: Poor people and people living paycheck-to-paycheck, particularly Black and brown people, are disproportionately affected by driver’s license suspension

- Only people who can’t afford to pay their debt are affected by debt-based driver’s license suspension.

- Communities of color are hit the hardest—in one Milwaukee neighborhood, 2 of every 3 working-age African Americans do not have a license.

Truth #6: There are better ways to promote debt repayment than suspending people’s driver’s licenses.

- The single most effective way to ensure compliance with debt is to reduce the debt to an amount that people can afford to pay. Jurisdictions that lower fines for people who can’t afford to pay them tend to see an increase in collections and a reduction in spending on enforcement. For instance, when one county decreased the fine amount in 90% of cases by an average of just $40, the average amount collected rose from $197 to $360.

- States have begun passing legislation allowing people to repay their debts using alternative methods, such as taking GED classes or participating in job training.

- We waste resources by using license suspension as a way to coerce payment from those who do not have the money to pay their debts. As a result, even after license suspension, the underlying debt often remains uncollected. As stated in the California Governor’s 2017-18 budget, “there does not appear to be a strong connection between suspending someone’s driver’s license and collecting their fine or penalty.”

Also, feel free to check out https://www.freetodrive.org/#page-content for more information.

Poverty Should Never Determine Who is Free to Drive

feel free to check out https://www.drivenbyjustice.org/

Please feel free to contact FFJC at (212) 431-2100 ext. 4310 if you have any questions or comments.

Leave a Reply