Beginning in 2008 the American Transportation Research Institute (ATRI) releases “An Analysis of the Operational Costs of Trucking” report. ATRI’s 2019 report documents the extremely robust economic environment that carriers and drivers experienced in 2018, with the caveat that these same conditions put significant upward pressure on nearly every line-item cost center experienced by carriers.

Therefore, the average marginal cost per mile incurred by motor carriers in 2018 increased by 7.7 percent to $1.82. Costs rose in every cost center except tires, with fuel costs experiencing the highest year-over-year growth of 17.7 percent. The alarming trend of insurance cost surges continued as the second-fastest year-over-year growth at 12 percent. In response to driver shortages that many companies experienced in 2018, driver wages and benefits increased 7.0 and 4.7 percent, respectively representing 43 percent of all marginal costs in 2018.

Not only are companies seeing a shortage of available drivers but there is a serious mechanic shortage as well. To that end repair and maintenance costs, at 17.1 cents per mile in 2018, have increased 24 percent since 2012, which seems counterintuitive given the record sales of new trucks and trailers. From 2012 to 2018, overall motor carrier operational costs have increased by more than 11.6 percent exceeding the 10.8 percent inflation rate for that same time period.

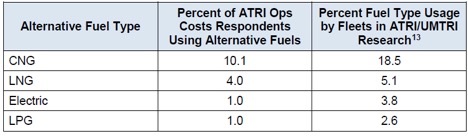

Something to track moving forward over the next few years is a push to alternative fuel vehicles. In 2018, 13 percent of carriers reported using alternative fuel vehicles (fuels other than diesel or biodiesel), a three percentage point increase from 2017 (see breakdown below). For many fleets diesel was more cost-effective but this is changing, not only due to continued rise in diesel ( $2.98 per gallon, while the equivalent amount of CNG cost $2.48 and the equivalent amount of LNG cost $2.71), but due to government intervention (through both incentives and disincentives), and the rise in e-commerce. As e-commerce increased local truck trips, overnight recharging of electric trucks is much more feasible, making them more viable.

(Source ATRI-Operational Costs of Trucking 2019)

(Source ATRI-Operational Costs of Trucking 2019)

Unsurprisingly, when breaking down operational costs by region Southwest and Southeast had the lowest operating costs in 2018. The highest costs were incurred by carriers operating predominantly in the West and Northeast (see below). The Northeast experiences heavy population concentrations and requisite traffic congestion and truck bottlenecks; these traffic conditions often come with increases in truck-involved crashes, generating higher repair, maintenance, and insurance costs. There is also a preponderance of toll roads in the Northeast, which is only getting worse as states such as Connecticut, Pennsylvania, and New York, to name a few, are salivating over increased tolling.

(Source ATRI-Operational Costs of Trucking 2019)

It must be said often and loudly, as trucking goes so goes the economy. Increased costs to the industry will trickle down to the consumers. Eventually, all piggy banks break.

Leave a Reply